State of the European Union

Policy recommendations for Europe

Build more science and technology clusters

According to the Draghi report, (i) the EU has only one science and technology (S&T) cluster (ranked 12) in the global ranking of the 20 largest S&T clusters of the world, and (ii) European companies have difficulties scaling up from startup to unicorn and beyond. Science and technology clusters are ecosystems that help new technology companies to hatch and grow by providing world-class research facilities, the proximity of a world-class higher education institution providing a talent pool, incubators and accelerators, growth capital, a favourable legislative framework, and first and foremost a vibrant community of entrepreneurs. Many of the global technology companies grew from such a cluster, and the fact that Europe has only one such cluster in the top 20 is problematic. Europe should therefore actively promote the creation of European S&T clusters in major urban areas and help them grow to a scale that they can support scaleup companies.

Introduce DARPA model of challenges

DARPA (Defense Advanced Research Projects Agency) in the US funds high-risk, high-rewards projects to generate transformative technologies. DARPA focuses on radical innovation and is willing to accept failure as part of exploring new ideas. Projects are quite short (two to five years) and must show measurable progress quickly. They are led by entrepreneurial programme managers who have a vision for technology breakthroughs, scout for innovative ideas, assemble the best teams and take corrective action if milestones are not met (including termination). This introduces a new R&D culture: fast, milestone-based, competitive, risk-tolerant, visionary, agile. Europe should use a similar model to tackle some of the grand challenges.

Stimulate pre-competitive procurement

A weakness of the current publicly funded research programmes in Europe is a failure to realize the full commercialization potential of research results. In many cases, the research results could be a good starting point for a spin-off company, but if nobody involved in the project has the ambition to start a company, the results are not commercially exploited. The reasons are well known: the principal investigators have a stable position in a research institute or company, and are not looking for an entrepreneurial adventure, and the goal of the PhD-students is to finish their PhD, not to create a company. Another barrier is that the gap between a proof of concept and a product is large, and researchers seldom have the business skills to close that gap.

Pre-competitive procurement follows a different approach. A government orders an innovative product or service that does not yet exist and creates a tender for a company or consortium of companies and universities / research and technology organizations (RTOs) to develop it.

This is how the world got COVID-19 vaccines: the first promising results of the phase I human trial were announced on 18 May 2020, that is, 137 days after the identification of the virus. The company was Moderna, a company only founded in 2010 in a sector where it is very difficult to bring a product to the market because it has to be clinically tested and approved by governments. Less than one year after the identification of the virus, the vaccination campaign was already rolled out at globally – this is the typical time between launching a call for research projects and the kick-off of the first projects.

Pre-competitive procurement not only shortens the execution time of the projects, but it also increases the likelihood of commercialization because delivering a working product or service is the task given to the consortium.

Background

In 2024, several reports were published on European competitiveness [1][2][3][4]. The conclusions are clear: the democratic shift, the restructuring of the global economy, and changing geopolitical relations are reducing the influence of Europe in the world. The world has become much bigger, while Europe remains fragmented, leading to a stunning_size deficit_ compared to the current global competitors from the US and China. This impacts Europe’s innovation capacity, productivity, job creation, security, … and in its wake the European political stability and eventually the European societal model. The solutions of the past might not be the most effective solutions for today’s (and future) grand challenges. The reports call for some fundamental changes to make Europe more competitive. This chapter investigates what can be done to make the European computing sector more competitive in the future.

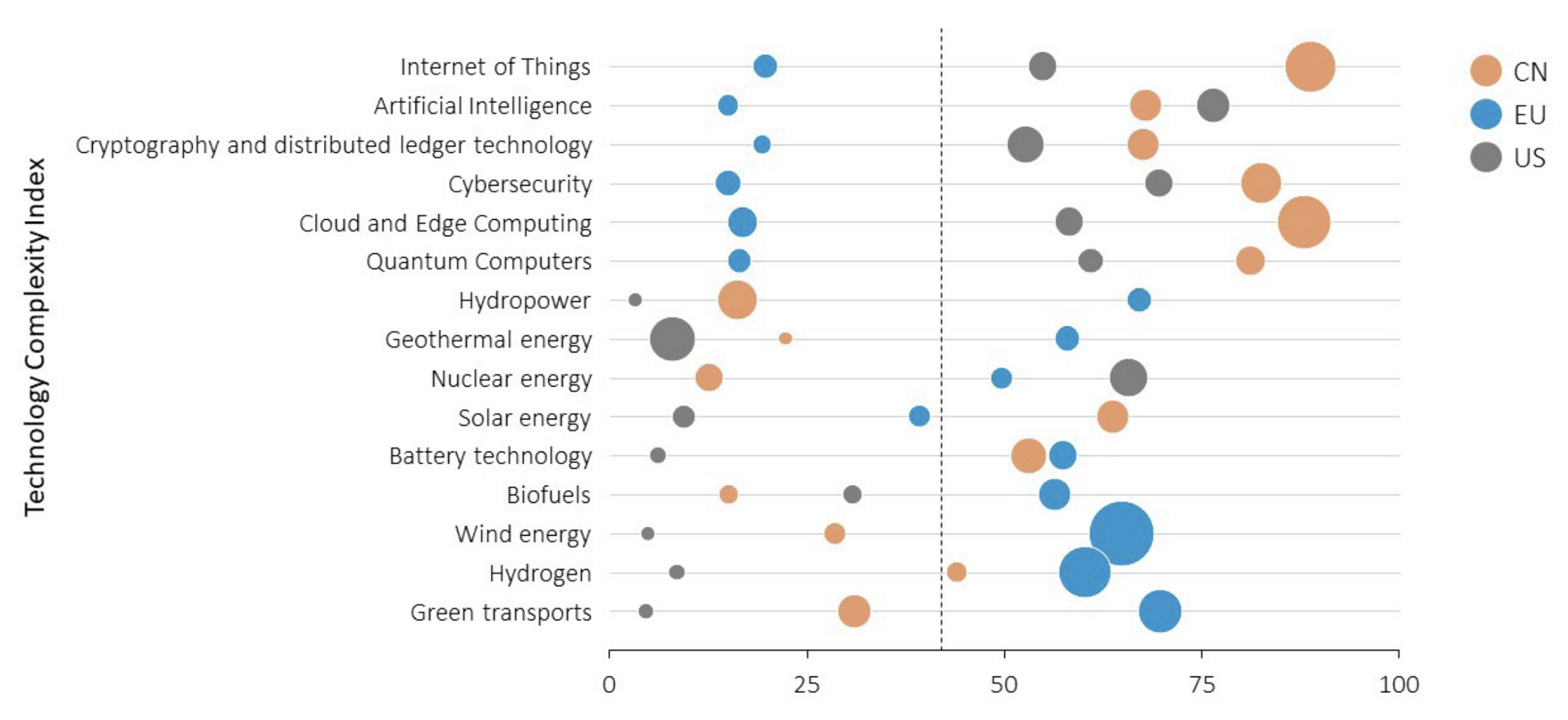

For the computing sector, today’s conclusions are dire. Despite all Europe’s efforts to boost research and innovation in digital technologies over the last two decades, Europe is seriously lagging behind the US and China in the domain of digital technologies. On the other hand, it is leading in the domain of sustainability technologies; see Figure 1.

Figure 1: Europe's position in digital and green technologies (2019-2022). The x-axis indicates how easily a country can build a comparative advantage. The size of the bubble indicates how strong it already is [1:1].

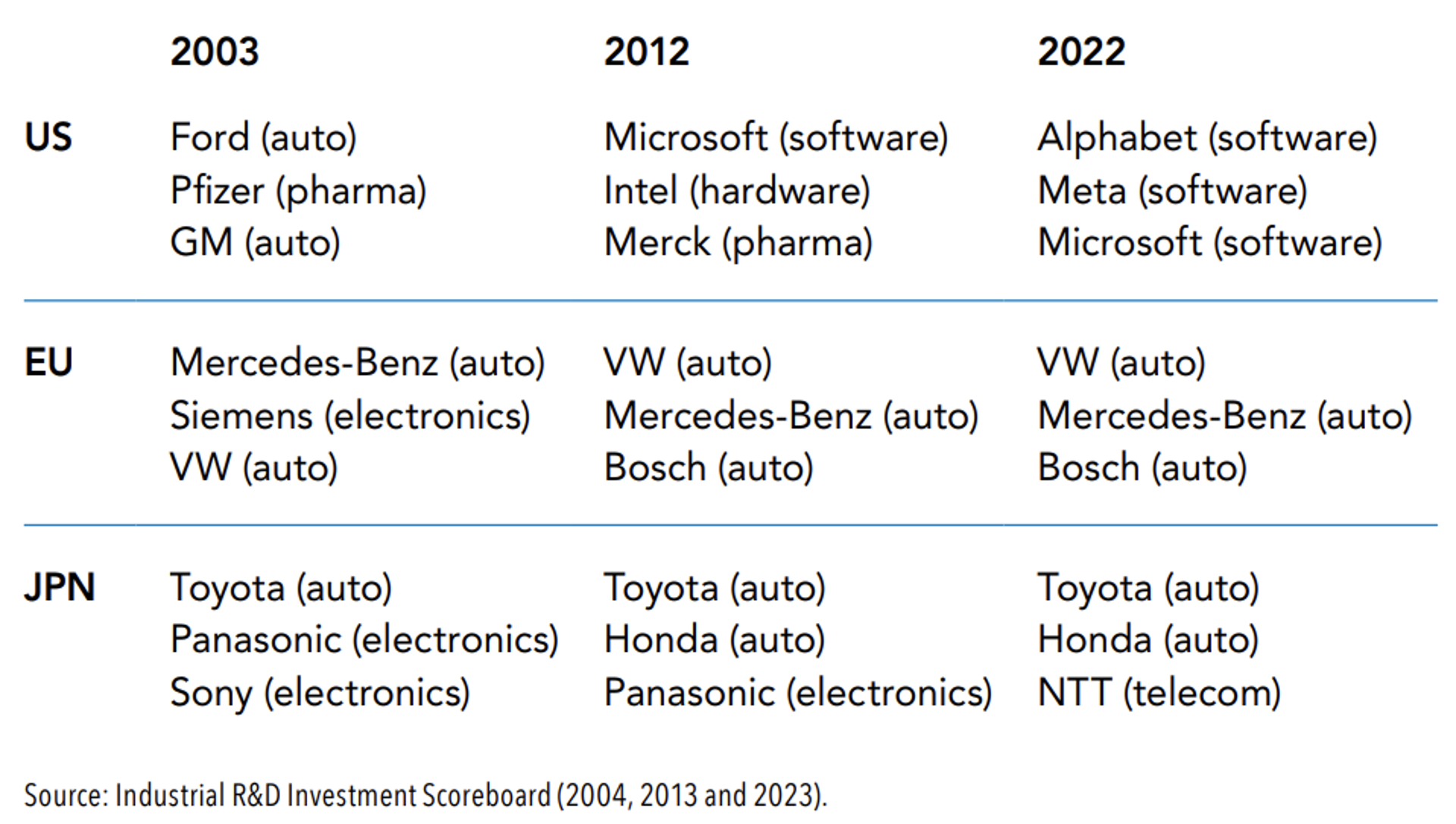

This is further illustrated in the Fuest report [5]. Table 1 depicts the biggest R&D spenders in 2003, 2012 and 2022 in the US, the EU and Japan.

While in 2003 automotive was king with five companies out of a total of nine, followed by electronics (three out of nine), in 2012 it was still five out of nine for automotive, but none were left in the US, and there was only one out of nine left for electronics, based in Japan. In the US, the biggest spenders in 2012 were Microsoft and Intel. In 2022, they have been replaced by Alphabet, Meta and Microsoft. The biggest spenders of 2012 in the EU are all automotive, and the same companies are still the biggest spenders in 2022. Not mentioned in the Fuest report are the three biggest R&D spenders in China in 2022: (i) Huawei investment and holding, (ii) Tencent, and (iii) Alibaba group Holding. These companies were founded in 1987, 1998, and 1999, respectively. The EU’s industrial innovation model is apparently more driven by established companies than in the US or China, where the leading companies in 2022 are much younger.

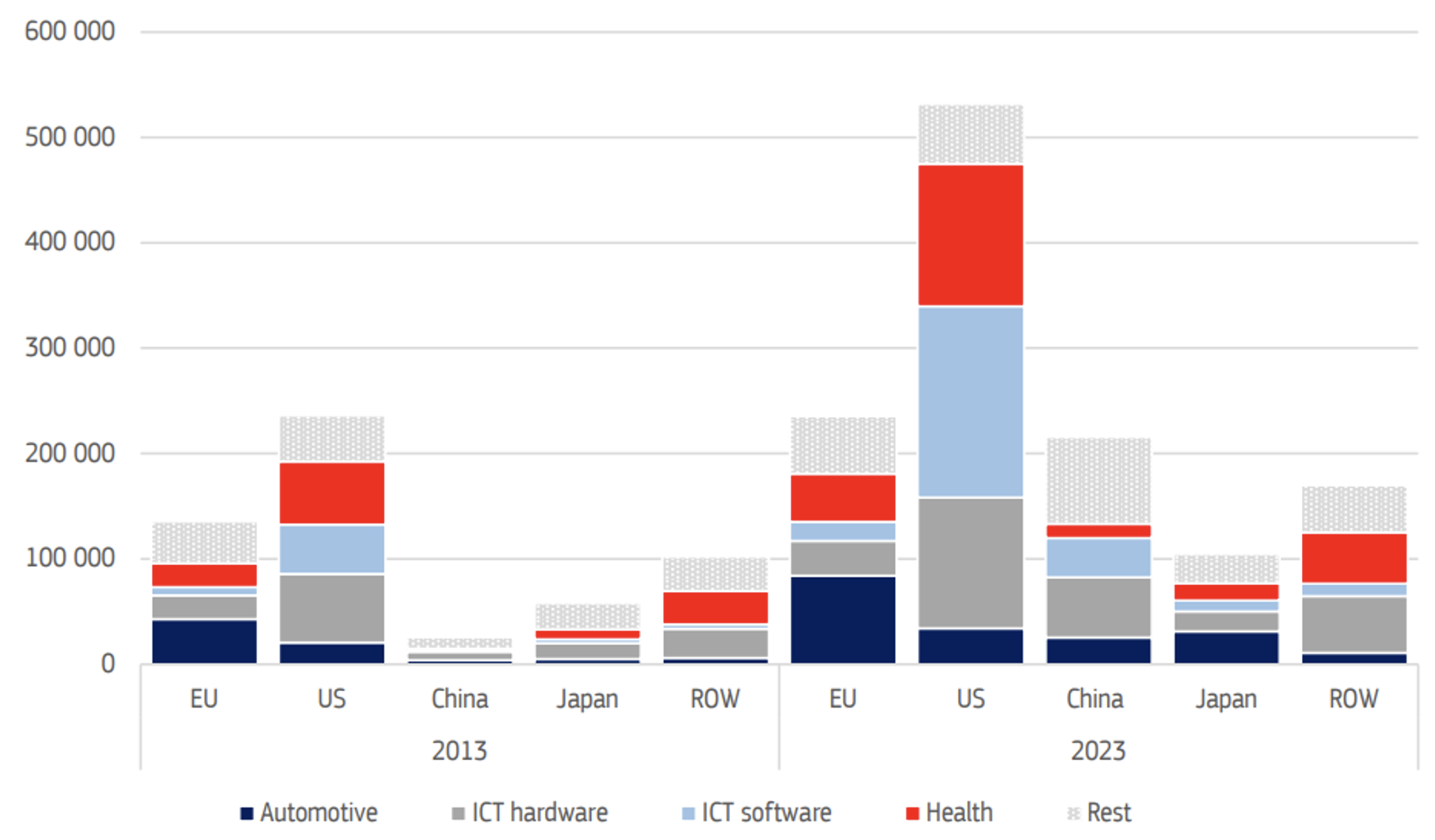

Figure 2 illustrates the private R&D investment evolution between 2013 and 2023 [6]. European industry almost doubled its R&D investments up to the level of US companies in 2013, but the US companies more than doubled their efforts at the same time, hereby doubling the gap between the two. In 2022, US companies spent the same amount of money on software R&D as the EU companies spend on software, hardware, health and automotive R&D combined. Chinese companies increased their investments eightfold over the same period and are currently almost on a par with the EU.

One third of the investments in Europe are coming from automotive companies, with limited investments by information and communication technology (ICT) companies (ICT hardware and ICT software), which are dwarfed by the investments by US and Chinese companies. The US companies invest 10x more in ICT software research than their European counterparts (up from 5.8 in 2013). At the current R&D investment levels, there is little chance that European industry will be able to catch up with US industry. The gap is simply too wide, and the resources available to close it are too limited.

Figure 2: Top R&D investments (in million euro) per sector in 2013 and in 2023 [6:1].

In 2024 several European automotive companies got into financial trouble and had to lay off employees and close factories, which could lead to a negative impact on their short-term R&D investments.

Also worrisome is that the European automotive sector seems to have difficulties competing with the US and Chinese market leaders in electromobility: Tesla and BYD. Tesla was founded in 2003 and sold its first car in 2008. In 2003, it was a startup, staffed by a handful of people. Since 2020 it has been the most valuable car manufacturer in the world. At the time that Tesla was (i) bringing its model S (2012) and its model X (2015) to the market, (ii) went public (initial public offering (IPO) in 2010), and (iii) introduced the Tesla Autopilot (2014), a major European automaker was trying to save its diesel car business by working on a cheat mode in the injection software. Although innovative, this is not the kind of innovation that will make Europe more competitive.

BYD Auto was also established in 2003. The first plug-in hybrid electric vehicle was launched in 2008, and the first battery electric vehicle in 2009. In 2023 Q4, BYD was the top-selling battery electric vehicle manufacturer of the world, bigger than Tesla. It overtook Volkswagen as best-selling car brand in China in 2023. It is the third most highly valued car manufacturer of the world, after Tesla and Toyota and followed by a series of European companies [7]. Traditional premium brands are seemingly less desirable in China now, with consumers switching to Chinese makes [8]..

From this limited analysis is clear that the US has been very successful in renewing its industry through so-called creative destruction. The decline of the automotive industry in what is now called the rust belt, has given rise to a much more innovative industry led by software companies like Alphabet (founded as Google in 1998), Meta (founded as Thefacebook in 2004) and Microsoft (founded in 1975). Their original mission statements were respectively: “organize all the world's information and make it universally accessible and useful", “to give people the power to share and make the world more open and connected”, and “to put a computer on every desk and in every home”, and this is exactly what they did, while also “mov[^ing] fast and break[^ing] things!”. Europe somehow seems to lack the ambition level that characterizes the US hyperscaler companies.

Science and technology (S&T) clusters

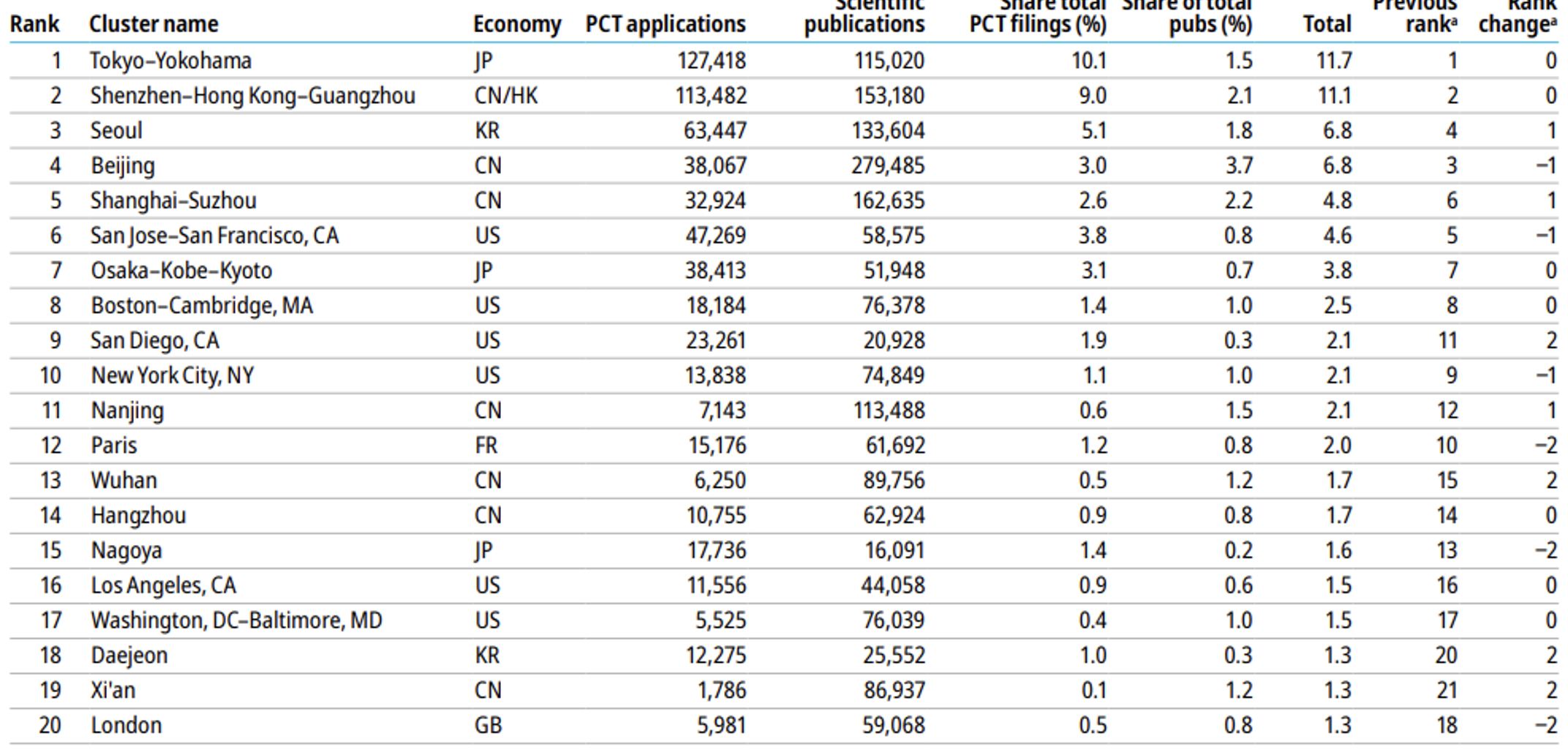

For startup companies to be founded, and once they are viable to scale up, they need an ecosystem in which they can find all the resources to grow: talent, infrastructure, investors, and a thriving entrepreneurial community. According to WIPO [9], in 2023, Europe had two science and technology (S&T) clusters in the global top 20; see Table 2. The metric used for the ranking is the share of the global patents plus the share of the global publications.

Paris is ranked no 12, and London no 20, but they both lost two positions compared to the 2022 ranking. The fact that Paris and London appear in this list is not surprising. They are the two largest metropolitan areas in Europe (with a population of more than 10 million), and an ecosystem can only grow large in a large metropolitan area. Other large metropolitan areas in Europe (Barcelona, Berlin, Madrid, …) are about half the size of Paris and London. Given the fact that the fast-growing cities with lots of young people are located outside Europe, the chance is low that Europe will be able to keep its position in the top 20 of global S&T clusters.

Knowing that S&T clusters are essential for startups to grow and thrive, Europe should actively encourage the creation of a multitude of medium sized S&T clusters in major urban areas in Europe. These will not land into the top 20, but they will be local innovation engines, creating well-paid jobs, stop brain drain and providing opportunities for the young generation. The performance per capita might even be higher than the S&T clusters in the top 20.

It is however important to realize that such clusters cannot be created overnight; they need time to grow and become productive, and they are always the result of joint efforts between different stakeholders.

- Local schools and universities must invest in research areas that are relevant for the local economy, and also develop the entrepreneurial skills of their students. This combination will result in spinoffs and startups, and it will also result in graduates that are ready to work in the local ecosystem (and attractive jobs in the local startups can stop them from looking for a job elsewhere). The schools and universities will also benefit from the ecosystem: contract research, company internships, and the ability to attract talented students who would like to work for one of the ecosystem companies.

- Local governments should offer ample space for high-tech companies to build the infrastructure they need and have a fast and pragmatic permissions policy. They should also arrange for affordable housing, an international school, efficient urban mobility and a liveable city.

- The (national and/or regional) government can create incentives to attract companies to designated areas (tax incentives, subsidies, …).

- Local companies must organize themselves too to make the infrastructure provided by the government into a vibrant and welcoming community in which all companies can learn from each other, help each other, celebrate successes, and especially grow the ecosystem, by e.g. investing in incubators, accelerators, ecosystem marketing, etc.

All the above needs time, but if all stakeholders (city, schools/universities, government, companies, …) in an area are willing to create such an ecosystem, synchronize their plans and investments, it can be built, and become the engine of economic development in the area. It takes time to produce the first big success stories (e.g. a unicorn), but once it reaches that level, and with the right marketing efforts, it will automatically attract talent and investors, and its growth will accelerate. All current large S&T clusters once started small.

Research excellence

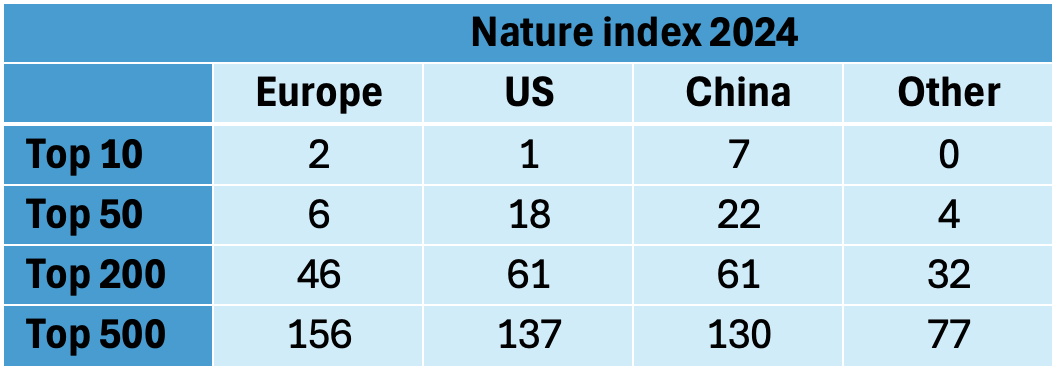

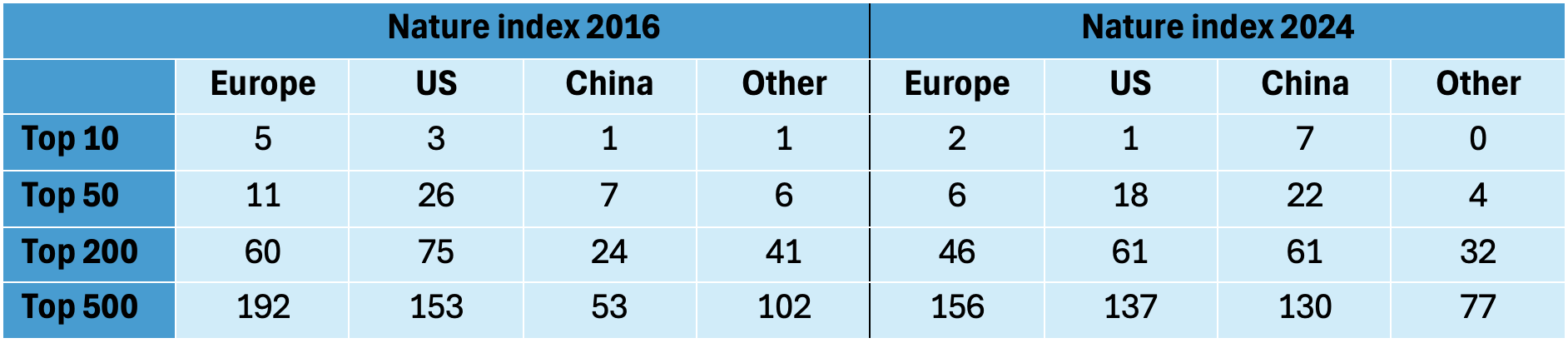

Europe not only lacks global science and technology clusters; it is also losing its position in basic research. The Nature Index tracks contributions to research articles published in high-quality natural-science and health-science journals, chosen based on reputation by an independent group of researchers; it has yearly updates. It can be used as a proxy for research excellence (just one possible proxy out of several). Table 3 shows the number of institutions in the Nature Index 2024 [10].

The top 10 in 2024 is dominated by Chinese institutions (70%), in the top 50, Chinese institutions are still 44% of all institutions, and Europe has only 12% of them. In the top 200, the US and China are on a par with 30% while Europe is at 23%. In the top 500, Europe leads with 31%. One could conclude that Europe does not lead in the excellent institutes (Top 50), but it clearly leads in the good ones (31% of the top 500 institutions). The group “Other” consist of mostly Asian institutions (Japan, South Korea, Singapore), Australia and Canada.

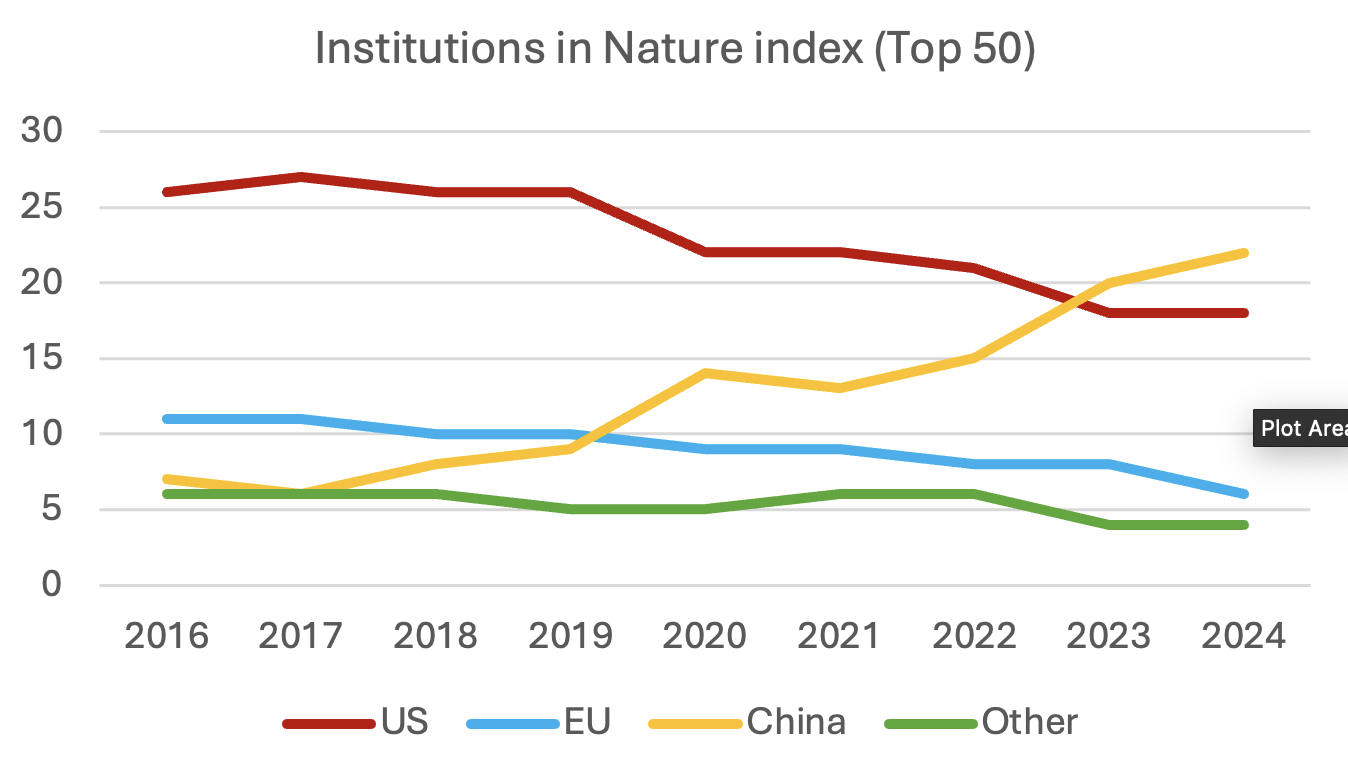

Figure 3, which plots the evolution of the top 50 over the last eight (!) years, put the 2024 situation in perspective: In less than a decade, Chinese institutions have succeeded in building a very strong position in the Nature Index. They have done so at the expense of Europe, the US and the rest of the world.

Figure 3: Evolution of the Nature Index Top 50, 2016-2024.

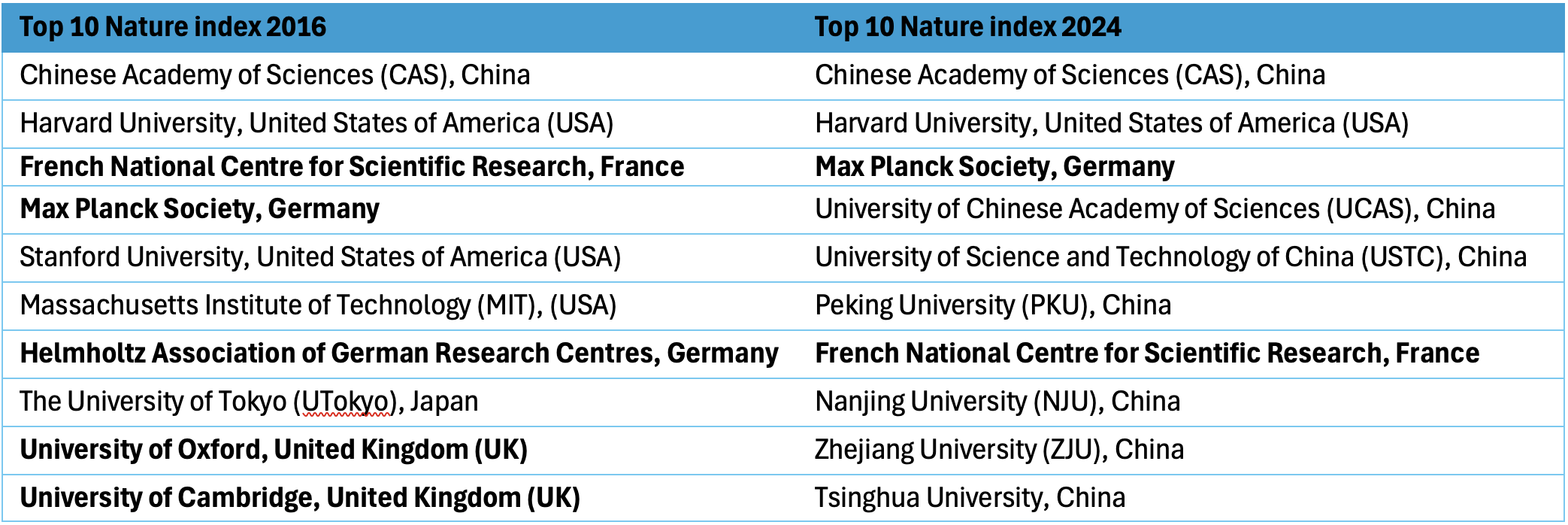

The seriousness of the situation becomes clear if we look at the detailed Top 10 in 2016 and compare it to 2024, as depicted in Table 3. Europe went in a timespan of eight years from five institutions to only two. The US from three to one. China grew from only one to seven out of 10. The fact that Oxford and Cambridge dropped from the Top 10 (Oxford is now at position 20, and Cambridge at 22) is telling for the new world order in research. China clearly ‘moves fast and breaks things’.

The full comparison is depicted in Table 5. It shows that the 31% of European institutions in the top 500 in 2024 was 38% in 2016, or a drop of 36 institutions in less than one decade!

One could argue that the Nature Index is not the most relevant index for ICT publications, but the submissions in ACM TACO (which reviews the papers for the HiPEAC conference) show a similar pattern: in 2016, it received 38 submissions from China out of a total of 199, while in 2024, there were 178(!) submissions out of a total of 303. In 2016, there were five accepted papers from China (acceptance rate 8% compared to 27% for the journal), while in 2024 there were 41 (acceptance rate 23%, compared to 31% for the journal). At the main paper track of the HiPEAC 2025 conference, 17 papers were presented by Chinese authors (out of 29). The Chinese research institutions have undeniably caught up with the US and the EU.

Why is this important? Excellent research feeds the innovation pipeline. Europe has a tradition of research excellence but has proven to be weaker in commercialization of the research (which often took place in the US). If Europe is losing its leading position in excellent research, it will inevitably have an impact on the innovation capacity of Europe in the long term. Applied to China, their recent research excellence will obviously create a huge potential for innovation and commercialization of innovative products. Figure 3 proves that 2024 is not an outlier, but the result of a trend that seems to be accelerating. The breakneck progress in AI makes this trend even more worrisome. If data science and AI becomes the engine of scientific discovery, the countries with the most data and compute capacity will have a competitive advantage.

So, the question is: where is Europe in this new world order, and how is it going to position itself? If Europe wants to stay commercially competitive, it will also have to stay competitive in research by unapologetically stimulating research excellence. One goal could be to have 20% or more institutions in the Nature Index which would come down to (2, 10, 40, 125) in the different rows of Table 5. This is lower than the numbers in 2016, but it takes into account that a new and ambitious player has entered the ranking, and the ranking is a zero-sum game.

Conclusion

After decades of investments in digital technologies in Europe, it made a lot of progress, but the US and China made even more progress, further increasing the gap. This is a wake-up call for Europe and suggests that the current European research and innovation policy is not adequate to keep up with Europe’s main competitors. This vision makes three recommendations to improve the situation.

- Europe should actively promote the creation of European S&T clusters in major urban areas and help them grow to a scale that they can support scaleup companies. This will stimulate the creation of innovative startups and retain talent in Europe.

- The DARPA model of challenges should be used to introduce a new R&D culture: ambitious, bold, fast, milestone-based, competitive, risk-tolerant, visionary, agile.

- Pre-competitive procurement should be used to speed up the introduction of innovative solutions to the market.

References

European Commission. The Future of European Competitiveness. By Mario Draghi, Publications Office of the European Union, 2024, https://commission.europa.eu/topics/strengthening-european-competitiveness/eu-competitiveness-looking-ahead_en ↩︎ ↩︎

European Commission. Much More Than a Market: Report by the High-Level Group on the Single Market, Chaired by Enrico Letta. Publications Office of the European Union, 2023, https://single-market-economy.ec.europa.eu/news/enrico-lettas-report-future-single-market-2024-04-10_en ↩︎

European Commission: Directorate-General for Research and Innovation. Align, Act, Accelerate – Research, Technology and Innovation to Boost European Competitiveness. By Manuel Heitor, Publications Office of the European Union, 2024, https://data.europa.eu/doi/10.2777/9106236 ↩︎

European Commission: Directorate-General for Research and Innovation, Science, research and innovation performance of the EU, 2024 – A competitive Europe for a sustainable future, Publications Office of the European Union, 2024, https://data.europa.eu/doi/10.2777/965670 ↩︎

Clemens Fuest, Daniel Gros, Philipp-Leo Mengel, Giorgio Presidente, and Jean Tirole: “EU Innovation Policy – How to Escape the Middle Technology Trap?” EconPol Policy Report, April 2024, https://www.econpol.eu/publications/policy_report/eu-innovation-policy-how-to-escape-the-middle-technology-trap ↩︎

European Commission: Joint Research Centre, 2024 EU industrial R&D investment scoreboard, Publications Office of the European Union, 2024, https://data.europa.eu/doi/10.2760/0775231 ↩︎ ↩︎

Julie Pinkerton, “The 10 Most Valuable Car Companies in the World By Market Capitalization”, USNews, 2024, https://money.usnews.com/investing/articles/the-10-most-valuable-auto-companies-in-the-world ↩︎

Mingyu Guan and Thomas Fang, “McKinseyChina Auto Consumer Insights 2024”, McKinsey, May 2024, https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/mckinseychina-auto-consumer-insights-2024 ↩︎

Global Innovation Index science and technology cluster methodology, https://www.wipo.int/export/sites/www/global_innovation_index/en/docs/gii-2023-cluster-methodology.pdf ↩︎

Nature Index, https://www.nature.com/nature-index/ ↩︎